Pricing and Charging

The aim of this work strand was to establish a framework for pricing and charging for access to equipment under the N8 Equipment Sharing agenda.

Objectives were set as follows:

- Identify a mechanism to ensure that the project is manageable and achievable;

- Define principles for a costing and pricing methodology that is accepted and equitable;

- Create a framework for charging that is accepted by funders as well as by academics, administrators and Facility Managers;

- Ensure the solution does not pose an unrealistic burden for individual HEIs;

- Define the above to comply with the following Key Principles:

- Simple and Transparent

- Approved by Funders

- Non-bureaucratic

Cost Models for Equipment Sharing

The Research Facility Cost Model used for the Transparent Approach to Costing (TRAC) is a good starting point for costing, is already an established mechanism for costing in the sector and, importantly, is approved by funders.

The Research Facility Cost Model provides the flexibility to deal with local differences in how facilities operate. This model gives a realistic picture of the total cost of running a facility and would allow for an accurate indication of what is required to make the facility sustainable, a key factor in how this initiative is taken forward.

Principles for Cost Inclusion

In line with TRAC Guidance for the costing of Research Facilities, costs can be included in the following groups:

- Pay Costs

- Non Pay Costs

- Replacement Cost Depreciation

- Space Charges where material

Utilisation levels should be defined as “Efficient Usage” as per TRAC.

Pay Costs – Definition of Direct Pay costs is relatively straightforward. Further guidance on the types of staff who might be included here is provided as part of the N8 EST. The N8 EST also highlights key things to consider as part of this data gathering.

Non Pay Costs – Definition of Direct Non Pay costs is also relatively straightforward. Further guidance on the potential categories of Non Pay costs is provided as part of the N8 EST. The N8 EST also highlights key things to consider as part of this data gathering.

Replacement Cost – A definition of Replacement Cost is given in the N8 EST. RCUK have left this largely to HEIs to define in stating that cost should be included for an appropriate specification of kit for the research to be carried out.

Depreciation – There has been considerable debate over the methodology for calculating lifespan and whether this should be open to institutional policy or defined by an agreement. It is recommended that Useful Life for the purposes of this calculation is defined by the Facility Manager. This allows for some flexibility to reflect local circumstances.

Space Charges – Space Charges should be included where material. This is in line with TRAC guidance for the costing of Research Facilities. For these purposes a suggested level of materiality at which these costs might be considered is 10% of total cost. The N8 EST gives some examples of how these might be calculated based on TRAC outputs.

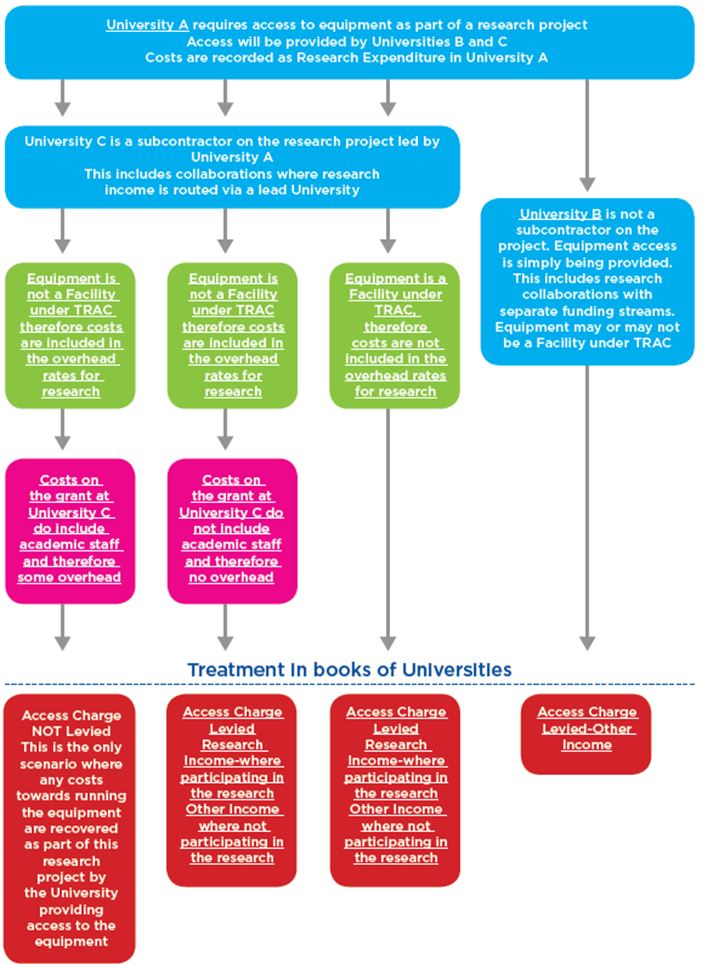

Price and Charging Pathways

Research Facility guidance is very clear in that price should be based on cost with no profit element built in. Adoption of the Research Facility Model above for price calculations ensures that this should be the case.

Pathways for payment for access to equipment fall into two broad areas:

- Where an institution is “selling” the use of a piece of equipment or facility;

- Where an institution is participating in the actual research, i.e. academic or research staff time is included as part of the bid.

The various routes and outcomes for charging are defined in the Charging Pathways Flowchart below and included as part of the N8 EST.